Are you looking to buy a Condo in Orange County, CA with a VA loan? There are things you need to know before starting the condo search that will help speed up the search process and relieve the potential frustration of finding out the condo you fell in love with is not eligible for a VA loan. The most important thing to know right out of the gate is that if you are using VA financing to purchase a condo, the condo project needs to be VA approved. And while it is possible to get a condo project VA approved after you have identified the condo you want to buy, it will be far easier to just limit your property search to only those condos that are in a VA approved condo project. But how do you do that?

Are you looking to buy a Condo in Orange County, CA with a VA loan? There are things you need to know before starting the condo search that will help speed up the search process and relieve the potential frustration of finding out the condo you fell in love with is not eligible for a VA loan. The most important thing to know right out of the gate is that if you are using VA financing to purchase a condo, the condo project needs to be VA approved. And while it is possible to get a condo project VA approved after you have identified the condo you want to buy, it will be far easier to just limit your property search to only those condos that are in a VA approved condo project. But how do you do that?

Two Ways to Search for VA approved Condos

There are two common methods used by Veterans and their real estate agents in searching for a VA approved condo. The most common method is to just look at ALL condos for sale and narrow down the search to the condos the Veteran is most interested in buying. Typically the search will be based on price range, bedrooms, bathrooms, size, location, etc. After filtering through 100’s of properties, anywhere from 3 to 30 properties may be identified as potential condos to buy. Then comes the frustrating part. Looking up each condo to see if it is eligible for VA financing. Since most condos in Orange County, CA are not VA approved, finding out that most of the homes are not even eligible for a VA loan is not only frustrating but a huge waste of time.

The far easier method is to only look at condos that are located within VA approved condo projects. And this is where it makes sense to work with real estate professionals who are familiar with the VA loan program and understand how to limit the search to only those properties eligible for a VA loan. The real estate agent can search the Multiple Listing Service (MLS) based on a narrowed down search of legal “Tract” numbers. The resulting properties are then forwarded to the Veteran, saving a ton of time (and frustration).

Another option for Veterans who want to do some searching on their own is to use a local VA Condo search website specific to Orange County. www.OrangeCountyVeteransHomes.com has done most of the legwork for you. There is a link for each city within Orange County. Simply click on the link and Bam, it’s done. For example, let’s say you are looking for VA approved condos in Irvine. By clicking on the Irvine link, a list of VA approved condos in Irvine will appear. As of today (Nov 19, 2020), there are 49 VA approved condos for sale with prices as low as $305,000 and as high as $1,030,000. A quick search for VA approved condos in Huntington Beach shows there are currently 20 properties for sale with prices ranging from $279,000 up to $800,000.

It is important to have an experienced Orange County VA loan specialist double-check the VA website to make sure the condo project is verified as approved because sometimes a condo project can run into financial issues or a lawsuit that can jeopardize their approval.

Buy VA Condo with $0 Down with No Limit in 2020

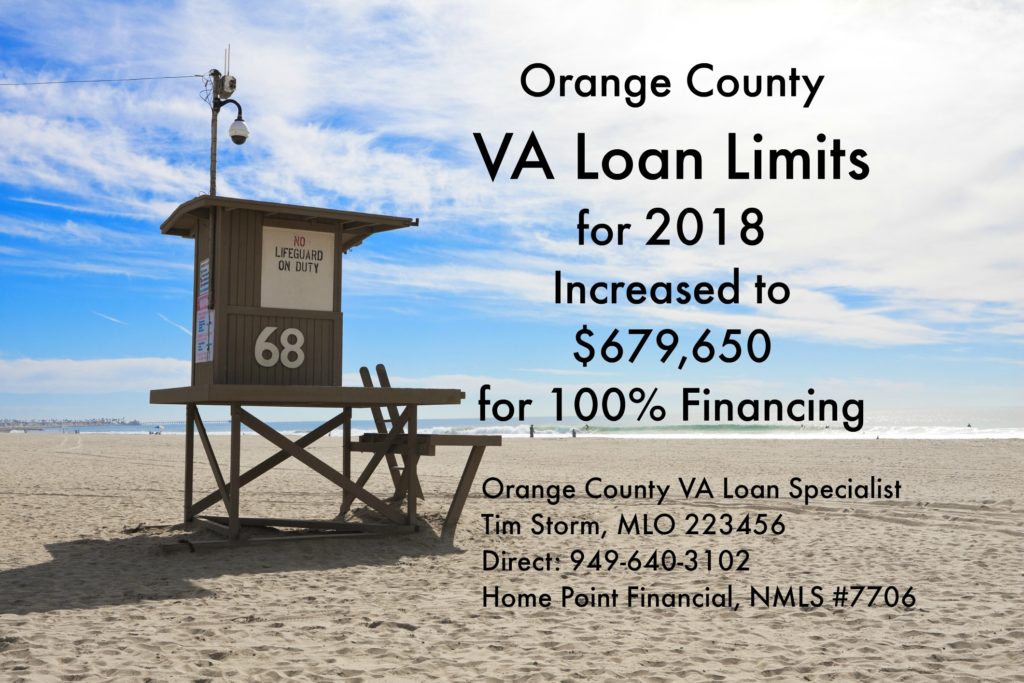

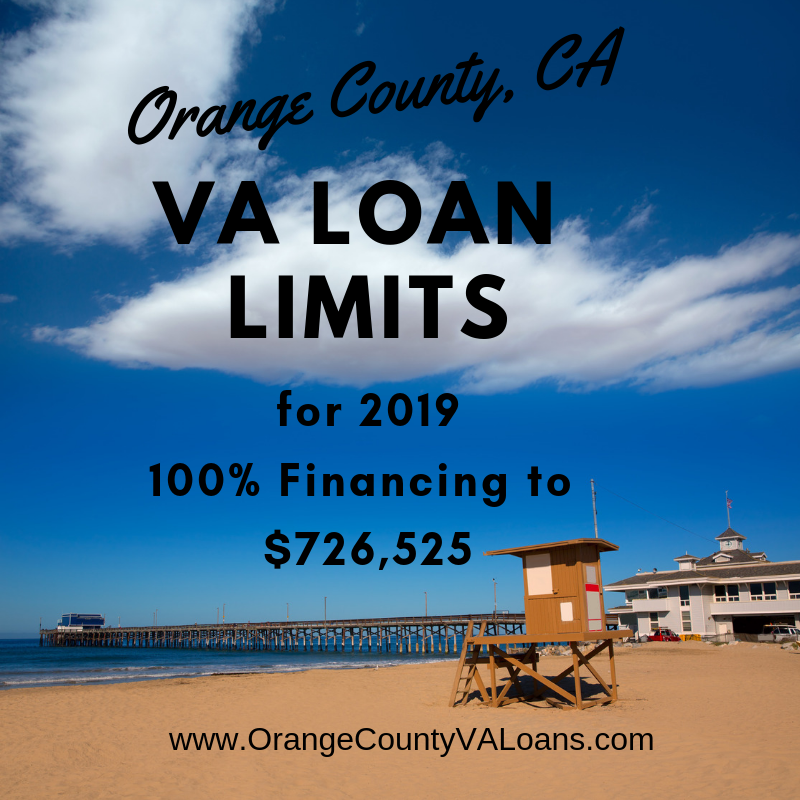

In 2020 VA will do away with loan limits for 100% financing. In the past, a Veteran would buy a home with ZERO down payment but only up to the county limit. In Orange County in 2019 the 100% financing loan limit was (is) $726,525. It was possible to buy a property and get a VA loan above that limit, but only with a down payment. Now, as a result of the “Blue Water Navy Veterans Act”, loan limits have been eliminated. This means that those high priced condos in Irvine and Huntington Beach, along with other upper-end areas of Orange County, a Veteran can buy with No Down payment.

In 2020 VA will do away with loan limits for 100% financing. In the past, a Veteran would buy a home with ZERO down payment but only up to the county limit. In Orange County in 2019 the 100% financing loan limit was (is) $726,525. It was possible to buy a property and get a VA loan above that limit, but only with a down payment. Now, as a result of the “Blue Water Navy Veterans Act”, loan limits have been eliminated. This means that those high priced condos in Irvine and Huntington Beach, along with other upper-end areas of Orange County, a Veteran can buy with No Down payment.

First Step in the Home Buying Process –VA Loan PreApproval

The first step in every home buying process should always be PreApproval. The last thing you want is to spend time finding the right property and then not be ready to make an offer. Most sellers will not accept an offer from a potential buyer who hasn’t talked to a lender yet and have a PreApproval letter in hand. With VA, it is important to work with a lender who specializes in VA. It is a unique program and working with a local Orange County Loan Officer who specializes in the VA loan program will help to make the overall process seamless. The VA Loan Officer will be able to pull the VA Certificate of Eligibility (you always want to make sure eligibility is clear before an offer is accepted), along with providing a Side by Side VA Total Cost Analysis (VA TCA). The VA TCA will give the Orange County Veteran a thorough breakdown of the numbers, making it easy to compare different options and price ranges.

Authored by Tim Storm, an Orange County, CA Loan Officer specializing in VA Loans. MLO 223456. – Please contact my office at Fairway Independent Mortgage Corporation. My direct line is 714-478-3049. I will prepare custom VA loan scenarios that will be matched up to your financial goals, both long and short-term. I also prepare a Video Explanation of your scenarios so that you are able to fully understand the numbers BEFORE you have started the loan process

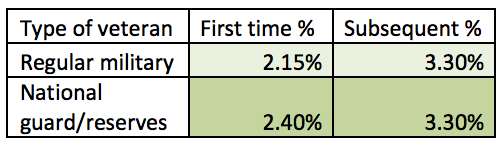

need to provide proof of service. Form 26-1880 may need to be completed if your lender is not able to get the COE on the first try. Also, the DD214 will need to be turned in to the lender if the COE is not retrieved on the first try. For the VA loan program, copy 4 of the DD-214 is preferred because it is the most detailed regarding your service. Reserve and National Guard members need to send in their most recent annual retirement summary with proof of honorable service attached. If you have been discharged from active duty and don’t have a proof of service form, you can still submit a request for a COE because in some cases the VA can determine your eligibility based on their own records.

need to provide proof of service. Form 26-1880 may need to be completed if your lender is not able to get the COE on the first try. Also, the DD214 will need to be turned in to the lender if the COE is not retrieved on the first try. For the VA loan program, copy 4 of the DD-214 is preferred because it is the most detailed regarding your service. Reserve and National Guard members need to send in their most recent annual retirement summary with proof of honorable service attached. If you have been discharged from active duty and don’t have a proof of service form, you can still submit a request for a COE because in some cases the VA can determine your eligibility based on their own records.

and Conventional loans both on average close in about 43 to 46 days (2017 statistic). On top of that VA loans are also more likely to close than a conventional loan. Because the VA loan program is a “niche”, Veterans should seek out lenders and loan officers who specialize in the VA loan program. An

and Conventional loans both on average close in about 43 to 46 days (2017 statistic). On top of that VA loans are also more likely to close than a conventional loan. Because the VA loan program is a “niche”, Veterans should seek out lenders and loan officers who specialize in the VA loan program. An